YEAR-OLD NORAZLAN ISMAIL, a taxi driver in Johor, embarked on a journey from Johor Bahru to Istana Negara.[1] Travelling on foot over six gruelling days during Ramadan in 2023, Norazlan sought to plead with national leaders to allow more Employees Provident Fund (EPF) withdrawals, so that he could pay off his debts. When questioned about his long-term financial security, the sole breadwinner replied: “Why should we think about the future when I feel like dying now?” Norazlan is one of many Malaysians forced to sacrifice long-term retirement security to resolve current financial hardship. As of August 2025, more than 4.6mil EPF members aged under 55 have withdrawn more than RM14bil via Account 3 (Akaun Fleksibel).[2] This means that 35% of EPF’s 13.2mil members have withdrawn at least RM3,000 from their retirement savings. The scale is such that one in four Malaysians could exhaust their EPF savings within five years of retiring.[3] Put more bluntly, retirement is slowly becoming a luxury. What has gone wrong, and what can be done to improve matters as Malaysia becomes an ageing nation?[4]

THE CURRENT RETIREMENT SAVINGS LANDSCAPE

The EPF is a mandatory bedrock of retirement for the private sector workforce and non-pensionable public servants. Largely funded by monthly deductions from employees (contributing 11% of their salaries) and employers (who top-up employees’ contributions by providing 12–13% of this figure), savings are invested in various financial securities to generate annual dividends (most recently declared at 6.15% for 2025).[5] Although the minimum retirement age has been raised to 60, contributors can begin withdrawing their savings at 55.

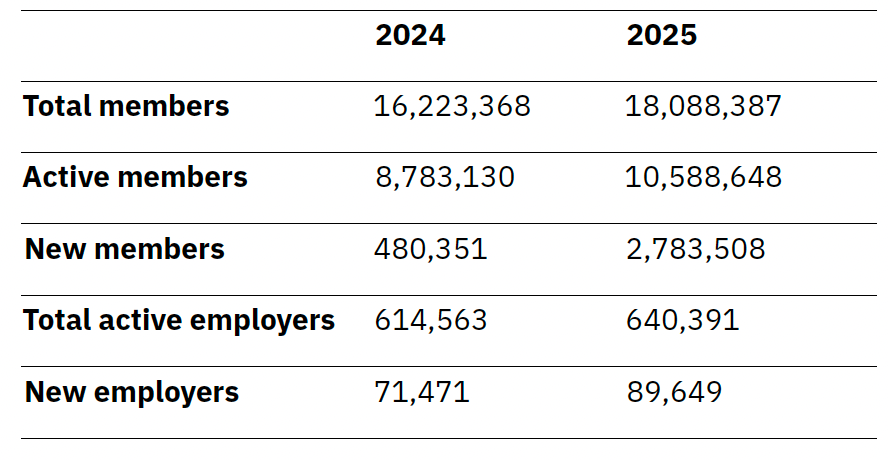

TABLE 1: EPF REGISTRATIONS, AS OF DECEMBER 2025[6]

In May 2024, EPF contributions were restructured as follows: 75% goes to Account 1 (Akaun Persaraan, the primary account); 15% to Account 2 (Akaun Sejahtera) for pre-retirement needs like housing and healthcare; and 10% to Account 3. While Account 3 was newly introduced to allow for emergency cash withdrawals, such as in Norazlan’s case, increased liquidity could risk prema-turely depleting vital savings (see Penang Monthly, June 2024). As of February, 74% of EPF members may have less than RM100,000 in savings upon retirement, an amount that could be depleted in fewer than five years.[7]